Sponsored by: ieso Health

Chronic diseases drive 90% of America’s healthcare costs. But most care programs miss addressing a key factor: mental health.

When anxiety and depression accompany chronic pain, cardiometabolic, gastrointestinal, or maternal health conditions, treatment adherence can drop, contributing to higher costs.

ieso’s clinician-designed mental health AI delivers evidence-based, personalized support, all while keeping users inside your chronic care program. Improve outcomes by caring for the whole person, not just the condition.

Want to sponsor the newsletter? Reach out. Now booking 2026.

My Reflection: $1,000 AI scans and US healthcare

I spent a few days in California this week leading a conversation with an executive team around the future of healthcare. One of the topics we found ourselves debating was whether the US healthcare system is the best in the world, despite its oft-discussed warts. An executive I was chatting with passionately argued that the US is indeed the best. His argument centered on access to high-end medical treatment in the US.

On my way back from California, I happened to see this excellent article in STAT by Katie Palmer that I thought served as an excellent example for this debate. The STAT article discussed how Medicare will likely reimburse AI-based coronary CT angiograms at over $1,000 per scan starting in 2026.

These seem like very cool, innovative tests. They’re offered by a handful of well-financed businesses, including Heartflow, Cleerly, and Elucid. It’s not hard to imagine the business opportunity here for those companies — the SaaS margins on an AI algorithm that generates $1,000 per use would seem quite attractive to investors. Elucid went so far as to issue a press release applauding the news. As an aside for this conversation, all of this is an excellent example of why I think the “AI will reduce the marginal cost of health care to zero” argument does not hold any water.

There’s a really compelling clinical narrative about the preventive nature of these screening tools. The financial calculus, particularly at $1,000 per use, is a little more unclear to me. You can see the financial calculus these companies use to justify the costs by articulating the savings that could be generated by avoiding downstream issues. Check out this quote from the STAT article: “If you could prevent that heart attack or stroke with a $2,000 cardiac CT angiogram with add-ons, you’re saving the health system $500,000 of care should that person with a heart attack actually survive,” said Elucid’s Huang.”

It’s hard to disagree with that logic. It does seem like expanded use of this technology will reduce heart attacks, which obviously seems great. Yet at the same time, I’m pretty confident that expanding access to this screening technology won't help reduce healthcare costs in this country. Quite the opposite, in fact. And that in so many ways encapsulates healthcare in this country.

We have access to so many incredible drugs, diagnostics, and devices that would have seemed like science fiction fifty years ago. For instance, it is bonkers to me that we can scan our arteries and use AI to identify plaque to prevent cardiac issues, as just one small example. Yet all of this innovation is also straining our collective ability to pay for these technologies as the companies behind them look to capitalize on the economic potential of creating them. It is our uniquely American approach to healthcare that has us in the cost crisis we’re in today. This leads me to a poll question for this week…

Poll of the Week

Back in 2017, The New York Times ran with a fun little healthcare policy tournament asking five health policy experts to pick the best health system in the world. Given the discussion above about the relative merits of the US healthcare system, I thought it’d be fun to revisit that question with this group.

Without giving away the full 2017 tournament results, I’ve offered the four semifinalists from 2017 as the four options below (US, Britain, France, and Switzerland), along with an “other” option. Will share the results next week.

In your opinion, is the US the best healthcare system in the world?

MEDICARE ADVANTAGE

Humana sues ChenMed, alleges it is siphoning tens of millions from joint venture JenCare

Beckers reported that Humana filed a rather interesting lawsuit last week against ChenMed for improperly taking money out of JenCare, a joint venture between the two organizations that operates MA-focused primary care clinics.

The core of the dispute centers on a technology licensing fee that appears ChenMed unilaterally imposed by ChenMed on JenCare without Humana’s consent in 2024. Humana argues this move was illegal, and ChenMed is effectively improperly funneling tens of millions of dollars in profits away from JenCare/Humana to itself.

Yet, while that is the issue presented in the lawsuit, it seems to be a symptom of a much broader simmering issue between the two parties. It’s pretty apparent from the lawsuit that there is bad blood between Humana and the Chen family at this point, with Humana at one point suggesting that JenCare was being treated as part of the “Chen family fiefdom.”

Reading between the lines of the lawsuit, it appears that the relationship deteriorated between 2015 and 2020, with the two parties having differing views on expansion plans for the JenCare senior clinics and the economics of that expansion. According to the lawsuit, Humana claims that ChenMed chose to grow its own clinic network rather than grant Humana additional equity in JenCare.

The relationship appears to have reached a breaking point around 2021, when the Chen family sought liquidity in its JenCare investment via an IPO. Humana objected. ChenMed proposed that Humana buy out ChenMed’s remaining interest in JenCare, apparently at an inflated price that Humana refused to pay. ChenMed then attempted to buy out Humana’s share with an unnamed private equity partner. Humana also balked at this because it was significantly lower in price.

As an aside, it’d be fascinating to see the math the private equity partner did behind this conversation — it’s not hard for me to envision that these clinics were worth substantially more if owned by Humana than otherwise, given how much of JenCare’s revenue was presumably coming from Humana.

After Humana balked at the M&A discussions, ChenMed resumed pursuing an IPO for JenCare in 2022, apparently without Humana’s knowledge. At this point, it appears the relationship deteriorated further and lawyers became involved, as Humana provided written notice to ChenMed regarding its improprieties. The two parties negotiated an agreement, signed in January 2023, that would give Humana protections against ChenMed’s related-party transactions in the event of an IPO. It appears this must have been part of the five-year network extension agreement that the two parties announced publicly in January 2023. It’s a good reminder of the chasm that can exist between how relationships can appear in the press and what they are like behind the scenes.

Around this time, it was also publicly reported that ChenMed was exploring a sale of its stake in JenCare. Business Insider reported in September 2022 that it was seeking a $4 billion valuation, roughly 3x the $1.3 billion revenue JenCare was reportedly generating at the time. Bloomberg later reported in September 2023 that Walmart was exploring acquiring a majority stake in ChenMed, valuing all of ChenMed at “several billion dollars”.

Per the Humana lawsuit, ChenMed began experiencing financial challenges in 2023 and 2024, and in late 2024, ChenMed decided to impose a technology license fee on JenCare, retroactive to January 2024. That move is what prompted the lawsuit here.

It’s fascinating to map that journey against the broader Medicare Advantage journey over the last decade plus, and think about the different decisions that both parties likely would / could have made along the way, knowing where the industry is today with v28. I’d imagine a significant portion of the valuation contemplated back around 2022 has evaporated — will be curious to watch if there is a path forward here for JenCare that remains.

STARTUP FUNDING

House Rx, a medically integrated dispensing model, raised $55 million

House Rx, a medically integrated dispensing model, raised $55 million this week, led by New Enterprise Associates and Town Hall Ventures (Town Hall’s thesis here).

House Rx partners with 1,000 providers across 80 clinics nationwide, up from 200 providers at the beginning of 2023. It currently processes $1.5 billion in specialty scripts and expects to be processing $3.0 billion by the end of 2026. House Rx appears to have been growing primarily in the oncology market (i.e. see its January 2023 partnership with Oregon Oncology Specialists), but also has expanded into rheumatology. If you peruse House Rx’s blog, you can start to get a sense of how it is finding traction — i.e. see this post talking about the practical issues that practices face in operating medically integrated dispensing models. It seems reasonable to me that a platform should help practices make this process more efficient, and that AI probably makes that process even more efficient.

The medically integrated dispensing model has seemingly been on the rise for some time, particularly in the oncology market. The percentage of community oncology practices with medically integrated dispensing apparently grew from 7.6% in 2010 to 28.3% in 2019. Those national percentages vary significantly state by state due to state laws, the penetration of networks like US Oncology, and whether hospitals have acquired community-based practices. The model has a certain logical appeal to it — moving prescribing closer to the provider to make access more timely for patients seems like a no-brainer, right?

Beyond its logical appeal, it seems this model has several strong tailwinds. Between the wave of state regulatory activism around PBMs, the cost and access issues people face, and the wave of pharma innovation, I’d imagine we'll hear more about medically integrated dispensing and similar ideas moving forward.

Chart of the Week

This Medicare Advantage enrollment update from Spark Advisors provides an early glimpse into trends in the MA applications Spark’s 8,000 brokers are processing as people enroll in new 2026 plans.

Notably, Humana and Devoted are seeing significant increases in applications, while UnitedHealthcare is seeing a significant drop. This chart sparked some fun dialogue in Slack about what this data actually means, how it’s only a partial view of overall enrollment trends, and you can’t extrapolate overall enrollment from this given it doesn’t provide any insights on disenrollments (or data beyond Spark’s experience).

With that caveat, the data does seem to support what Humana reported on Q3 earnings — that Humana’s enrollment was pacing at the high end of its expectations, and likely that Devoted is going to be in a similar situation as well with meaningful growth. It’ll be fascinating to see where these numbers end up, particularly for the big movers here.

Other Top Headlines

Amazon One Medical announced that Montefiore will become its primary specialty partner for its fifteen clinics in Manhattan, expanding on a partnership announced earlier this year to open clinics in Westchester County and surrounding areas. It appears that Montefiore is replacing Mount Sinai as One Medical’s preferred partner in Manhattan, given One Medical and Mount Sinai originally announced a partnership in New York City in 2019. It’s interesting to think about the give-and-takes of a change like this — I’d imagine the switch is about financials first and foremost, but it also seems like a pretty meaningful change for the One Medical customer base.

Minnesota-based health system Fairview is in the middle of two rather interesting contractual disputes at the moment, one with UnitedHealthcare and one with the University of Minnesota. Fairview and UHC are at an impasse in renegotiating a contract that expires at the end of 2025. UHC says that Fairview is requesting a 23% rate increase for commercial plans, which would result in $121 million in extra payments going to Fairview. Fairview says that UHC’s demands would force it to choose between cutting services and limiting access to care. Meanwhile, Fairview and the University of Minnesota are at an impasse, with the University of Minnesota objecting to what it calls a “hostile takeover” of its medical school by Fairview. I suppose some days you’re the dog, some days you’re the hydrant.

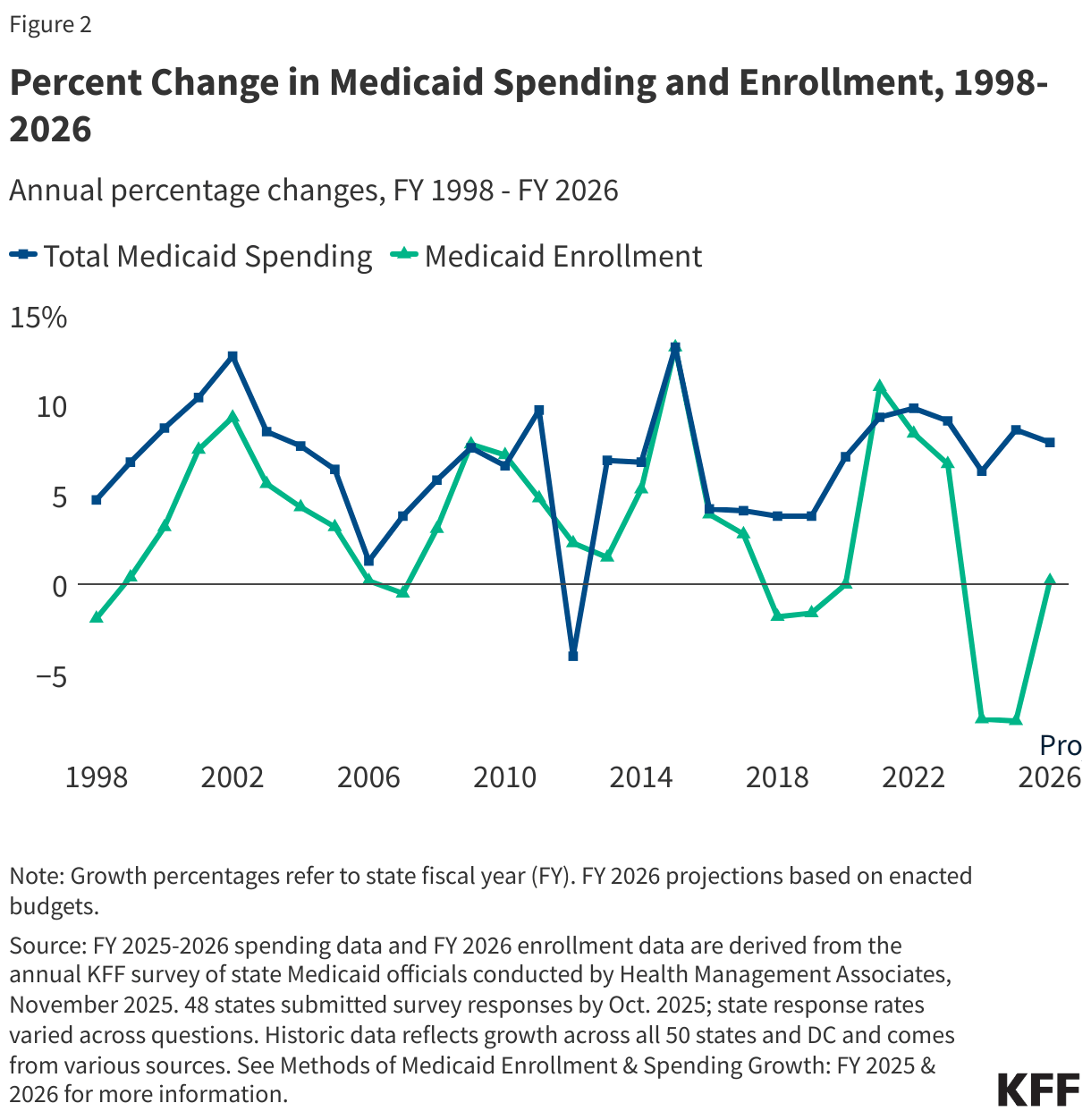

CMS issued new guidance on Friday evening regarding Medicaid payments, closing a timing loophole that states were attempting to use to increase taxes that draw on matching federal funds. CMS noted it expects to save taxpayers $200 billion over ten years by closing this loophole.

Virtual care platform Fabric announced its fifth acquisition this week. It is acquiring UCM Digital, a virtual care provider with 400 payer and employer clients covering 1 million lives. Fabric notes it now serves 75 health systems, 30,000 employers, and 100+ million lives across the US.

Bloomberg reported this week that Elevance has sued New York City over its recent decision to move its health benefits administration to other insurers at the end of the year.

Luma Health announced it acquired Tonic Health from R1 RCM.

Featured Jobs

Director, Growth Strategy & Operations at Habitat Health, delivering care to older adults through a Program of All-Inclusive Care for the Elderly (PACE). Learn more.

$160k - $190k | Hybrid (SF)

Associate Director, Virtual Health at Privia Health, a physician enablement company. Learn more.

$105k - $120k | Remote

Manager, Enterprise Marketing at Progyny, a benefits management company for family building and women’s health. Learn more.

$90k - $110k | Remote

Senior Manager, Consulting at Dana-Farber Cancer Institute, a cancer treatment and research center. Learn more.

$143k - $165k | Hybrid (Boston)

Strategy & Operations Lead, RCM at Prosper Health, virtual mental health services for autistic adults. Learn more.

Hybrid (NYC)

Contact us to feature roles in our newsletter.

This Week on HTN

Here’s a round-up of our other content from the last week:

What I’m Reading

Lessons from Pandemic Medicaid Automation for Work Requirements by Luke Farrell

A fascinating look at the work the United States Digital Service performed supporting state Medicaid agencies after the pandemic, and the implications for implementing work requirements. Read more.

I Canceled My Family's Health Insurance (and joined CrowdHealth) by Nat Eliason

This post shares Eliason’s decision-making process in joining CrowdHealth, a crowdfunding platform for healthcare expenses. While I can definitely understand the financial rationale, this whole conversation makes me extremely queasy. It seems reasonably easy to predict what will happen here — models like this will appear to work great until all of a sudden they don’t, with unfortunate consequences for people who expect this to cover them. Read more

Machine Gods: On crises of faith, slop, and the art of medicine by Chukwuebuka Anyaegbuna

This was an interesting — and rather philosophical — read on the future role that doctors can play with AI. It references Coatue’s investment thesis in OpenEvidence from earlier this year, which is a good read in its own right that I hadn’t seen before. Read more

Funding Announcements

House Rx, a medically integrated dispensing model, raised $55 million. See discussion above.

Clairity, an AI platform for breast cancer imaging, raised $43 million.