Washington, D.C.

The first round of ACCESS Model Accepted Participants was released this week. We’ve talked about ACCESS a lot around the HTN offices, in the HTN Slack, and to our friends and loved ones who only seem to reply with sighs and grimaces.

My take, for what it’s worth, is that:

It is hard to save money on health care due to Baumol’s cost disease and the fact that all the interested parties will suffer consequences from any reductions in health care spending, which inevitably translate into some combination of lower revenue, less access, or worse quality.

If we want to avoid raising taxes or reducing benefits, we need AI (or some other technology) to help us solve the productivity problem and/or change the calculus of these interested parties.

I have some, what I think is, healthy skepticism that AI is going to necessarily enable infinite healthcare, or fully automated luxury

communismhealth care.But this is precisely the sort of thing we want the CMS Innovation Center to test!

The CMS Innovation Center describes its mission as:

The CMS Innovation Center develops and tests health care payment and service delivery models to improve patient care, lower costs, and align payment systems to promote patient-centered practices.

I say this in the most laudatory way, but CMMI is a very American attempt to resolve the tension in the Gallup poll I screenshotted above. Should the government raise revenue or reduce costs? The American people pretty decisively say no, so we created CMMI to try to come up with a third option.

Looking through the list, I was pleasantly surprised by the number of companies that raised their hands for what seems like a sort of Project Hail Mary1. I think we’ll still end up having to either raise taxes or reduce benefits, but I think it’s cool that we’re trying, and the expected value, despite the low probability, is still very high because we spend so much on health care.

Elsewhere in Washington:

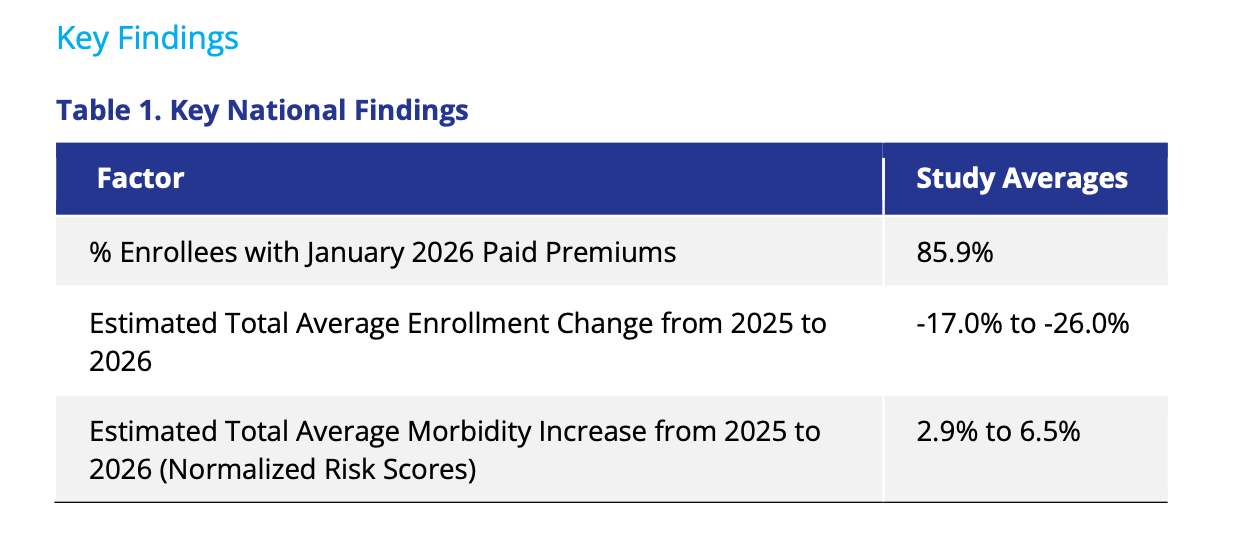

While we wait for effectuated ACA data from CMS, Wakely’s Who Paid, and Who Stayed? Early 2026 Enrollment Trends in the Individual Market provided a nice read-through based on their data. Smaller and sicker, but less contraction than the public markets were expecting:

IPPS and LTC proposed rule factsheet here: The proposed increase in IPPS payment rates is projected to be 2.4%. This reflects a projected FY 2027 hospital market basket percentage increase of 3.2%, reduced by a 0.8 percentage point productivity adjustment. Also proposes expanding the Comprehensive Care for Joint Replacement (CJR) Model to mandatory and nationwide

New Chernew just dropped in Health Affairs Forefront: Levels, Growth, And Semantics: The Role Of Prices In Driving Health Care Spending, a rebuttal to Papanicolas et al’s The US Health Spending Problem Is Still About Prices, which itself was a rebuttal to Chernew’s Growth In National Health Expenditures: It’s Not The Prices, Stupid

State Capitols

An idea you hear sometimes is that health insurance should work more like car insurance. Usually, the person advancing this argument is mostly talking about the ACA’s essential benefits, comparing health insurance paying for annual physicals to car insurance paying for an oil change.

It’s an interesting thought experiment, but there are a couple of rejoinders you tend to hear by way of response: One flavor is about the merits of the essential health benefits themselves, either in reducing longer-term costs (an ounce of prevention is worth a pound of cure) or a political one where the voting public really doesn’t like paying premiums, having high deductibles, and not getting any sort of first-dollar coverage.

Another flavor of criticism of this metaphor is that health insurance markets and car insurance markets differ in some pretty important structural ways. The two big ones are that (1) driving without car insurance is illegal, or practically illegal, in nearly every state, and (2) car insurers are allowed to underwrite based on individual driver characteristics like age, history of accidents, and cetera.

(Interestingly, the ACA tried to adopt (1) with its individual mandate while making (2) mostly illegal, instead only allowing insurers to use “community rating” based on geography, wide age brackets, and smoking status.)

A challenge with the car insurance structure that might be nagging you if you live in a place in the United States with only limited public transport options is that some people are both a bad risk from an insurance perspective but need to drive to work, bring their kids to school, and cetera.

States devised a clever solution to this problem: assigned risk pools, which do pretty much what it sounds like. People who couldn’t otherwise can’t get car insurance apply through a state-operated program, and they are assigned to an insurance company that must accept them, but can charge them higher prices than a standard customer. This balances the insurer’s ability to profitably manage risk with people, even poor drivers, legitimate need for car insurance.

I find this to be a pretty satisfying way for a state to solve a market failure. In a pre-ACA world, states tried to do something similar for people deemed uninsurable in commercial plans, though the general consensus is that they didn’t work very well, and the ACA’s guaranteed issue provision made them irrelevant. It does seem to work better for Workers’ Comp, where states spin up an insurer of last resort company, which can end up being a pretty good business you can then spin out for a cool $300m if things get tight in the budget.

Another somewhat obscure corner of a state’s insurance obligation is providing Medicaid to foster children and young adults who have aged out of the foster care system, or at least it was obscure to me before reading this article in KFF titled “State-Run Insurance Plans for Foster Kids Leave Some of Them Without Doctors.”

North Carolina is one of 14 states with such specialized foster care plans, according to the National Academy for State Health Policy. The plans differ by state, but each is meant to expand coverage for children in the foster care system — and for kids who were adopted out of it, such as Ollie and her siblings.

Yet, as in other states that have struggled when adding such plans, North Carolina families have faced hurdles obtaining care. Thousands of doctors whose services were covered under Medicaid were not included in the specialized plan — which is costing the state $3.1 billion over four years — when it rolled out on Dec. 1. That left guardians and parents of kids adopted out of the system scrambling to figure out whether they would have to find new health care providers or new insurance.

Reading through the article, many of the challenges KFF identified, like not covering CAR T-Cell Therapy, limited provider networks, and inadequate mental health services, strike me as tragic, but unfortunately, rather garden-variety tragic, Medicaid problems. In short, eminently solvable problems that are unfortunately only solvable with more money.

Bracketing those problems for a moment, a state-facilitated special needs plan holds a lot of promise, with the state having a unique interest in the continuity of care, and foster-impacted children and young adults having a unique set of needs. Of course, we can’t really bracket the problems; an underfunded special needs plan doesn’t really accomplish much for those impacted by the foster system and might not be any better or even somewhat better than traditional Medicaid or an MCO. But it would be a really cool thing if a state could pull it off.

Elsewhere at the state level:

HCPF has a new executive director, Gretchen Hammer, who was Colorado’s Medicaid Director from 2015-2018 and most recently worked for Mathematica as a Senior Fellow.

The Maryland state legislature sent a bill to the governor’s desk: “Requiring certain insurers, nonprofit health service plans, and health maintenance organizations to provide coverage for screening for perinatal health conditions at certain times; requiring certain health care providers to screen for perinatal behavioral health conditions; requiring the Maryland Department of Health to identify certain screening tools and to assist certain health care providers with accessing resources and referral services related to screening for perinatal behavioral health conditions; etc.”

This NYT article (gift linked) makes for an interesting read on how state and local policymakers are thinking about the implementation of the community engagement requirements. It notes two exemptions: medical frailty and high unemployment.

Modern Healthcare reminded me that Nebraska is implementing community engagement requirements on May 1st, 2025 or 15 days from today. As of Sept 2025, Nebraska had about 72k expansion members, roughly 65% who meet the criteria for the community engagement requirements. KFF had a nice overview of Nebraska Medicaid and how it varies in implementation from OBBBA via a state plan amendment

More from Health Tech Nerds

Weekly Health Tech Reads

April 13th, 2026: A musing on 2027 Final Notice, a payor / provider spat between Jefferson and Aetna, Teladoc's valuation issues, BCBS MN's financial issues, and more. Read here.

HTN Radio: YouTube; Apple Podcasts; Spotify

The Grand Roundup: CMMI's LEAD program and engaging specialists via CARA, MA final rates and benefit cuts, Teladoc's valuation conundrum, AI creating confusion in private markets, and SimpliFed's $10.8M Series A to extend OB care.

Making GLP-1s work for patients and payers | Evan Richardson (Form Health).

Improving pediatric care access and outcomes through value-based Medicaid contracting, technology, and a prevention-first model | Chris Johnson & Michael Glazier, MD (Bluebird Kids Health).

Every Monday: The Grand Roundup Live

Want to comment or share feedback?

If this newsletter was forwarded to you, subscribe here or see more from Health Tech Nerds.

1 I’m only halfway through the book and haven’t seen the movie, so sorry if this metaphor isn’t apropos