Washington, D.C.

How should prices be set in health care? The economic marketplace theory is basically that you get buyers (doctors) and sellers (patients) in a room; they bargain, agree on a price, and eventually the market clears: sellers and buyers pair off, creating a market price.

This happens in some corners of health care, but it isn’t at all universal. Sometimes, the buyers of healthcare are, for example, gunshot victims who aren’t really in a position to shop or bargain. If you’ve been shot in the chest, you are pretty much a price taker, so the price discovery mechanism breaks down. Similarly, some people don’t have insurance, but we’ve decided as a country that hospitals should still be required to treat them, so sometimes a provider is required to be a price taker, in this case, the price being what the industry euphemistically refers to as uncompensated care.

There are lots of little and big ways that price discovery and normal market mechanisms break down in health care; probably the biggest perversion is the third-party payer system we have. Because prices are so high and most people most of the time have not been shot in the chest or have some horrible cancer, it makes sense to pool risk via insurance. So insurance companies are doing the bargaining with the doctors rather than with individuals. In response, providers have grouped together in medical groups and hospitals because, in this case, market power is really what determines the price. This gets a bit “snake eating its own tail” because the high prices beget consolidation, which begets high prices, but it’s also hard to imagine a world without third-party payers.

A weird quirk of this third-party payer system, where the price discovery really breaks down, is that for idiosyncratic reasons, most hospitals use contract labor for things like anesthesiology or to staff doctors in the ER, so, for example, sometimes the insurance company and the hospital will have an agreement, but the anesthesiologist does not. Since these contract laborers often form what I think you could fairly call, in the economic sense and with no value judgment attached, something approximating a cartel, the prices the provider charges are quite high.

The No Surprises Act, among other things, was designed as a remedy, and from a patient’s perspective, it’s worked quite well. I have gotten a surprise bill from an anesthesiologist, replied to said bill with the DC Office of Health Care Ombudsman and Bill of Rights in carbon copy, saying basically, “you aren’t allowed to do that,” and the matter was resolved.

But from an insurance company’s perspective? Not so much. Sarah Kliff and Margot Sanger-Katz in the New York Times (gift-linked):

Dr. Norman Rowe, a plastic surgeon with offices in New York and Florida, advertises on his website that breast reduction surgery usually costs between $15,000 and $25,000.

But these days, his practice sometimes earns $440,000 for the procedure.

Dr. Rowe has taken full advantage of a new arbitration system, part of a major consumer protection law Congress passed in 2020 with bipartisan majorities. The No Surprises Act was designed to eliminate surprise medical bills, for patients who showed up in the emergency room and were treated by a doctor who didn’t take their insurance.

It bars those out-of-network doctors from billing patients directly. Instead, they can plead their case to a government-approved arbitrator. If they win, the patient’s insurer has to pay their desired amount.

By all accounts, the law is successfully protecting patients against bills from doctors they never chose. But it has also generated an expensive unanticipated consequence: Doctors have flooded the arbitration system with millions of claims. Most are winning, often collecting fees hundreds of times higher than what they could negotiate with insurers directly or what they could have earned from patients before the law passed.

If you can get an 18-29x premium for a procedure through the IDR process, you’re probably going to go for it. But it strikes me as a real tragedy of the commons situation where the next policy iteration is going to involve some sort of price setting, maybe Medicare rates or a percentage of Medicare rates, which, uh, I don’t think they’ll be wild about.

Elsewhere in Washington

BALANCE is on hold for Medicare with Aetna and UnitedHealthcare out, the GLP-1 Bridge program from CMMI is being extended.

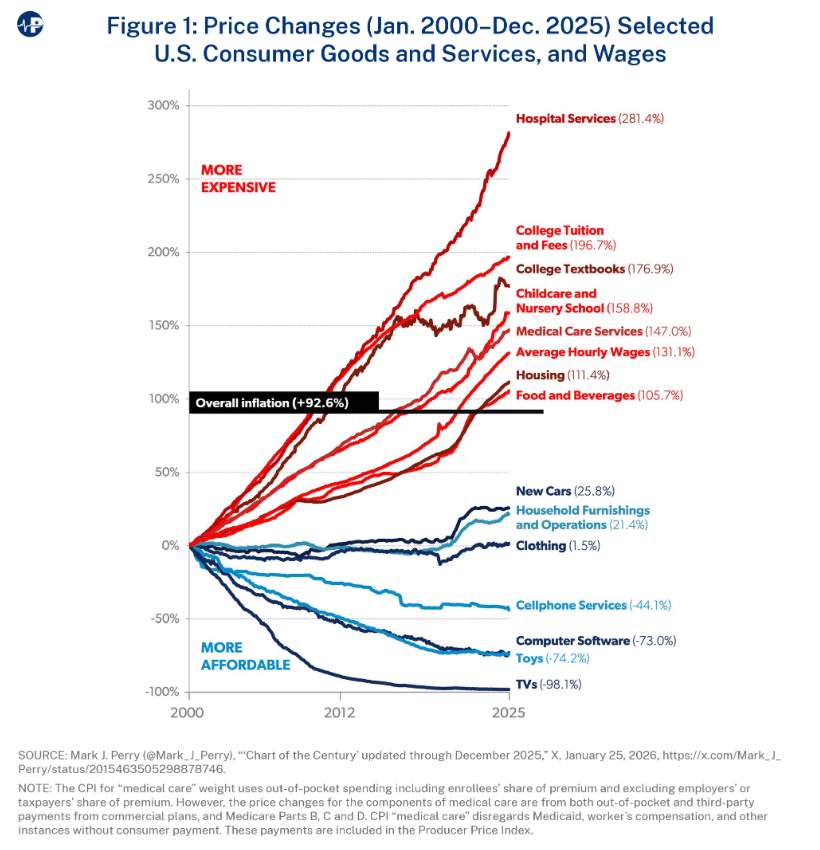

Trump administration aligned health care think tank The Paragon Institute released The Hospital Cost Crisis paper which recommends reforms like “such as site-neutral payment, stronger price transparency and subsidy oversight, repeal of anticompetitive rules, targeted charity-care standards, and restructuring hospital support programs to reward quality, efficiency, and genuine need.” It also included this graph, which is a pretty neat illustration of Baumol’s cost disease.

Writing in Health Affairs Forefront, Ellen Breslin and Dennis Heaphy share an agenda for CMS to strengthen coverage for dual-eligible adults with behavioral health needs.

State Capitols

When you hear the term “public option” with respect to American health care, you are completely forgiven for checking the calendar to make sure it isn’t 2009. The substantive portion of the debate over an American public option has been over since the Senate Democrats left it out of what became the Patient Protection and Affordable Care Act.

The mechanics of this sort of public option are simple. Rather than a single-payer situation (like France) or a market of private plans (like Switzerland), the government would operate a health plan that competed with private plans in the market. A certain sort of market-oriented Democrat finds this to be an aesthetically pleasing solution to some of the market failures of a pure single-payer system or private market approach. The public option becomes a de facto rate setter that the private plans can free-ride on, but the public option doesn’t need to throw off profits, so the private plans really have to be more efficient than the government plan. A nice feature of this system is that it requires less regulatory scrutiny of health insurance plans since the public option, in addition to being a price setter, also acts sets service standards. If the public option has a good network, limited prior auths, and a well-staffed call center, the private plans need to have those things too, to effectively compete.

Or at least that’s the theory. There are a lot of ways you can imagine it going sideways. The closest thing we’ve got as a test case is sort of the reverse with Medicare adding a private option in the form of Medicare Advantage, but the analogy isn’t perfect and there isn’t much of constituency in Washington, D.C. for a public option. The left wing of the Democratic Party is focused on Medicare For All, Republicans seem to be coalescing around HSAs and ICHRA, and there aren’t many folks eager to pitch a sort of weird, disruptive hybrid that health insurers and hospitals would both hate.

Confusingly, at the state level, legislators in Washington state, Colorado, and now, Nevada, have been experimenting with something they call a public option, but it isn’t, really. Rather than the state operating a plan that competes with private insurers, states ask, cajole, or jawbone private or non-profit health plans to offer a “public health insurance option” and then require them to meet premium reduction benchmarks.

In Nevada’s case, they required the Medicaid Managed Care Organizations in the state to submit bids, sort of a “nice MCO business you got there, be a shame if something happened to it” situation.

I try to check my personal biases and beliefs at the door on matters of health care policy and financing, so I feel the need to admit to a certain fondness for the Berkeley public option paper, which had a big impression on me in my youth. For that, and other reasons, I’ve tended to take a pretty dim view of these not even quasi-public options at the state level. What is, essentially, telling the insurance companies that they better save money just doesn’t seem like it would work very well.

But as I set about researching to write this week’s HPB, I read a report from Colorado’s Division of Insurance prepared by Mathematica and you know what, in very heavily caveated and nuanced terms still very early on in the experiment, it seems like it does: “Relative to average premiums for non-Colorado Option consumers in 2022, these effects correspond to a decrease of 3.4 to 7.8 percent.”

CO DOI report prepared by Mathematica

These aren’t life-changing dollar amounts or anything, but they are real, statistically significant savings relative to the non-public option plans on offer. In a moment where substantive health care policy innovation at the federal level seems unlikely, it will be interesting to watch states see what they can do.

Elsewhere at the state level

“CMS will require all states to submit a plan within 30 days outlining how they will verify that healthcare providers are real, licensed and actually delivering care under Mediciad, particularly in areas flagged as high-risk for fraud.” (Beckers)

States want the administration to review proposed changes to the essential health benefits again. (Inside Health Policy)

Medicaid Managed Care Procurement Reveals Systematic Overemphasis of Technology and Equity Performance Claims Across 32 States (Journal of Healthcare Organization, Provision, and Financing)

Medicaid breakthrough comes with unexpected immigration mandates (North Carolina News)

More from Health Tech Nerds

Every Monday: The Grand Roundup Live

Weekly Health Tech Reads

4/20/26. ACCESS rates, more fun with peptides, early data on ACA morbidity, and the Keytruda investigation. Read here.

HTN Radio

Want to comment or share feedback?

If this newsletter was forwarded to you, subscribe here or see more from Health Tech Nerds.